To download the Auspice March Blog, click here.

In Q1 2025 equities came under moderate selling pressure. As of March end, the S&P500 had an approximate 10% peak to trough drawdown and is down 5% year to date. Auspice has outperformed, protecting capital in Auspice Diversified and even delivering positive performance in Auspice Broad Commodity and linked ETFs (COM/CCOM).

What about the strong, double-digit performance Auspice Diversified has delivered during prior equity corrections? “Crisis Alpha” typically occurs during meaningful equity selloffs. When equity markets first start to turn over from highs, trends in equities and other economically sensitive markets are often in transition. As corrections become more meaningful, liquidity driven trading, emotions, and “risk-off” typically leads to non-correlated trend following opportunities.

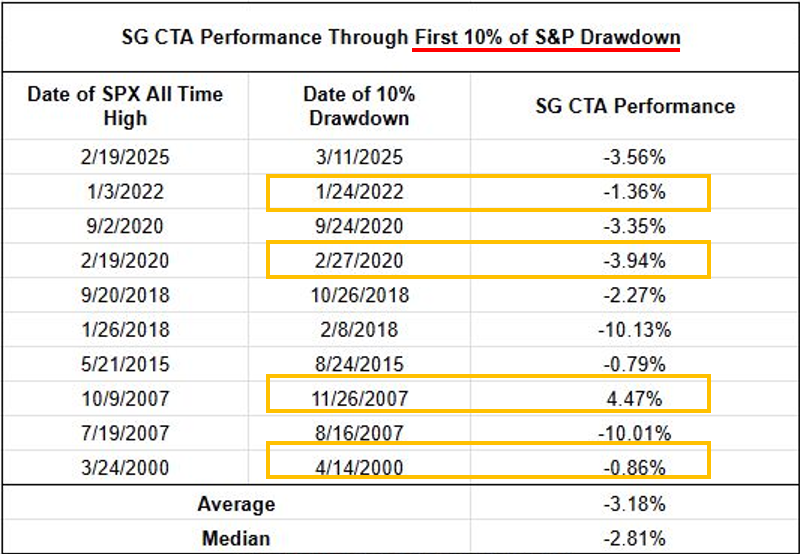

Consider Table 1 below with historical SG CTA performance during the first 10% of a S&P 500 drawdown. As you can see, our financially focused CTA peers have on average lost 3% when the S&P 500 has traded down 10% from highs. While negative, CTA peers deliver a better result than equity beta.

Table 1: SG CTA peer performance through the first 10% of a S&P 500 drawdown:

Source: DBi and Auspice. You cannot invest directly in an index.

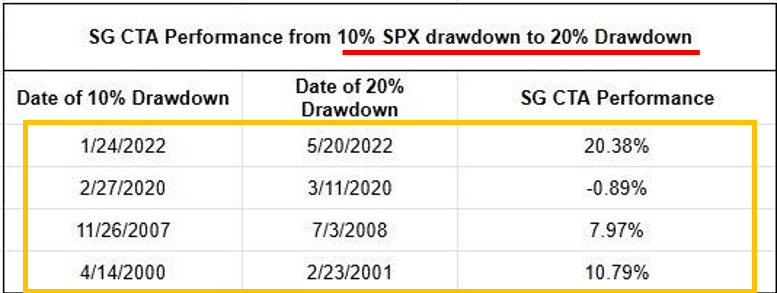

However, as a selloff becomes more significant, trend-following CTAs have been a reliable source of crisis alpha. Note the gold boxes in Table 1 above. In these four periods the S&P 500 correction reached 20%. As you can see below in Table 2, performance during these meaningful corrections is strong.

Table 2: SG CTA peer performance when S&P reaches -20%:

Source: Potomac and Auspice. You cannot invest directly in an index.

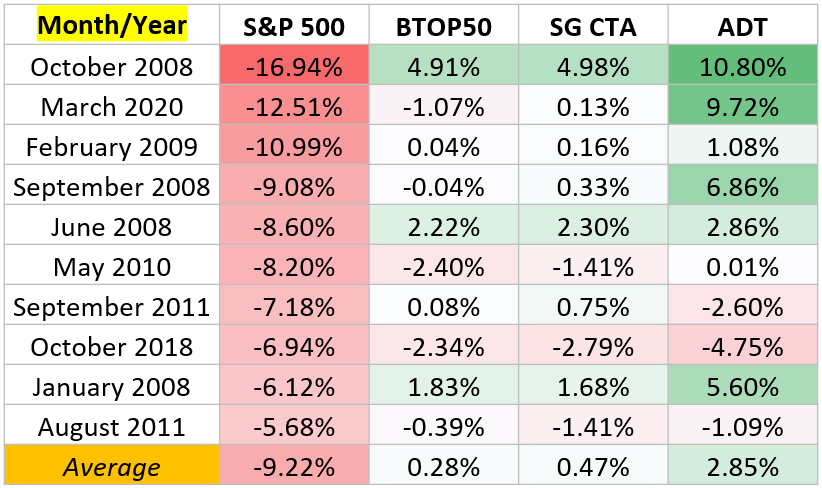

A similar pattern is observed if we look at the worst 10 months and worst 10 quarters for the S&P 500 since 2007 (Auspice Diversified inception). See Table 3 below. In the worst 10 months, the average performance of the S&P 500 is -9.2%, a moderate or even routine correction. Our CTA peers do well on average, protecting capital with the BTOP50 and the SG CTA benchmarks up +0.3% and +0.5% respectively. Auspice Diversified on the other hand outperforms, up an average of +2.9%.

Table 3: BTOP50 CTA, SG CTA, and Auspice Diversified performance during the worst 10 S&P 500 months:

Source: Auspice Capital and Bloomberg. You cannot invest in an index.

As equity selloffs become pronounced, we see stronger crisis alpha from both CTA peers and Auspice Diversified – strong offsetting performance when you need it most. See Table 4 below.

Table 4: BTOP50 CTA, SG CTA, and Auspice Diversified performance during the worst 10 S&P 500 quarters:

Source: Auspice Capital and Bloomberg. You cannot invest in an index.

You may have noticed we often refer to “crisis alpha”, but not “tail hedge”. Tail hedge typically has a much more negative equity correlation, approaching -1.0. Tail hedge is typically expected to deliver strong offsetting performance with a high degree of reliability, albeit also with negative long-term returns. This has proven not practical and uninvestable for most investors.

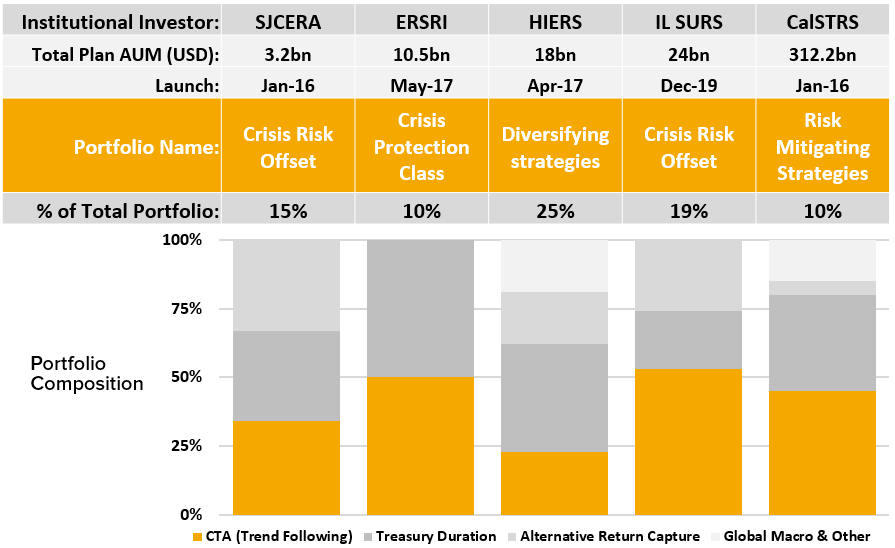

Table 5: Trend Following CTAs receive 5-10% of many US pensions long term asset allocation.

Source above: “The Institutional Use of Commodities & CTAs”, Auspice. Published November 2021 and data as of then. SJCERA is San Joaquin Country Employees’ Retirement Association. ERSRI is Employees’ Retirement System of Rhode Island. HIERS is the State of Hawaii Employees’ Retirement System. Illinois SURS is the State Universities Retirement System of Illinois. CalSTRS is California State Teachers’ Retirement System.

What will happen going forward? We do not have a crystal ball. Auspice strategies have a defensive positioning today with positive performance recently as equities continue to come under pressure. But the recent lag versus equity recent is historically normal and often followed by a pop in the right direction.

If you don’t have a 5-10% allocation to CTAs strategies, or are not at your target weight, now may be an opportune time to rebalance out of recent equity strength and into CTAs. For further information email us today at info@auspicecapital.com.

DEFINITIONS

Indexes

· The Standard and Poor's 500, or simply the S&P 500, is a stock market index tracking the stock performance of 500 of the largest companies listed on stock exchanges in the United States.

· BTOP Index (Barclay CTA Index): The BTOP Index is a benchmark for managed futures programs, specifically tracking the performance of the largest Commodity Trading Advisors (CTAs) who employ systematic, trend-following strategies. It is constructed and maintained by BarclayHedge and aims to reflect the representative performance of active CTA managers.

· SG CTA Index (Société Générale CTA Index): The SG CTA Index is a performance benchmark for the largest CTAs selected by Société Générale, based on assets under management. It includes 20 CTAs and is equally weighted and rebalanced annually, representing a broad view of the managed futures industry.

IMPORTANT DISCLAIMERS AND NOTES

There is a substantial risk of loss in trading futures and options. Past performance is not necessarily indicative of future results.

The returns for Auspice Diversified Trust ("ADT") are “net” (including management and performance fees, interest and expenses). Returns represent the performance for Auspice Managed Futures LP Series 1 (2% mgmt, 20% performance) including and ending November 2019. From this point, returns represent the performance for Auspice Diversified Trust Series X (1% mgmt, 15% performance) which started in July 2014.

The indicated rates of return are the historical annual compounded total returns including changes in share and/or unit value and reinvestment of all dividends and/or distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any securityholder that would have reduced returns.

Some of the assumptions and opinions contained herein are the view or opinion of the firm and are based on management's analysis of the portfolio performance.

Prior to February 28, 2023, Auspice Diversified Trust was offered via offering memorandum only and this Fund was not a reporting issuer during such prior period. The expenses of the Fund would have been higher during such prior period had the Fund been subject to the additional regulatory requirements applicable to a reporting issuer. Auspice obtained exemptive relief on behalf of the Fund to permit the disclosure of the prior performance data for the Fund for the time period prior to it becoming a reporting issuer.

Commissions, trailing commissions, management fees and expenses may all be associated with investment funds. Please read the prospectus before investing. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

The contents on this website are provided for informational and educational purposes and are not intended to provide specific individual advice including, without limitation, investment, financial, legal, accounting and tax. Please consult with your own professional advisor on your particular circumstances.

Futures trading is speculative and is not suitable for all customers. Past results are not necessarily indicative of future results. This document is for information purposes only and should not be construed as an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice. Auspice Capital Advisors Ltd. makes no representation or warranty relating to any information herein, which is derived from independent sources. No securities regulatory authority has expressed an opinion about the securities offered herein and it is an offence to claim otherwise. Please read the offering documents before investing.

Certain statements in this document are forward- looking statements, including those identified by the expressions “anticipate”, “believe”, “plan”, “estimate”, “expect”, “intend”, “target”, “seek”, “will” and similar expressions to the extent they relate to the Fund and the Manager. Forward- looking statements are not historical facts but reflect the current expectations of the Fund and the Manager regarding future results or events. Such forward-looking statements reflect the Fund’s and the Manager’s current beliefs and are based on information currently available to them. Forward-looking statements are made with assumptions and involve significant risks and uncertainties. Although the forward-looking statements contained in this document are based upon assumptions that the Fund and the Manager believe to be reasonable, neither the Fund or the Manager can assure investors that actual results will be consistent with these forward-looking statements. As a result, readers are cautioned not to place undue reliance on these statements as a number of factors could cause actual results or events to differ materially from current expectations.

The forward-looking statements contained herein were prepared for the purpose of providing prospective investors with general educational background information about the Funds and may not be appropriate for other purposes. Neither the Fund or the Manager assumes any obligation to update or revise them to reflect new events or circumstances, except as required by law.

This blog may contain hypertext links to web sites owned and controlled by other parties than Auspice. We have no control over any third-party-owned web sites or content referred to, accessed by or available on this web site and therefore we do not endorse, sponsor, recommend or otherwise accept any responsibility for such third-party web sites or content or for the availability of such web sites. In particular, we do not accept any liability arising out of any allegation that any third-party-owned content (whether published on this or any other web site) infringes the intellectual property rights of any person, or any liability arising out of any information or opinion contained on such third-party web site or content.